")

")

Introduction

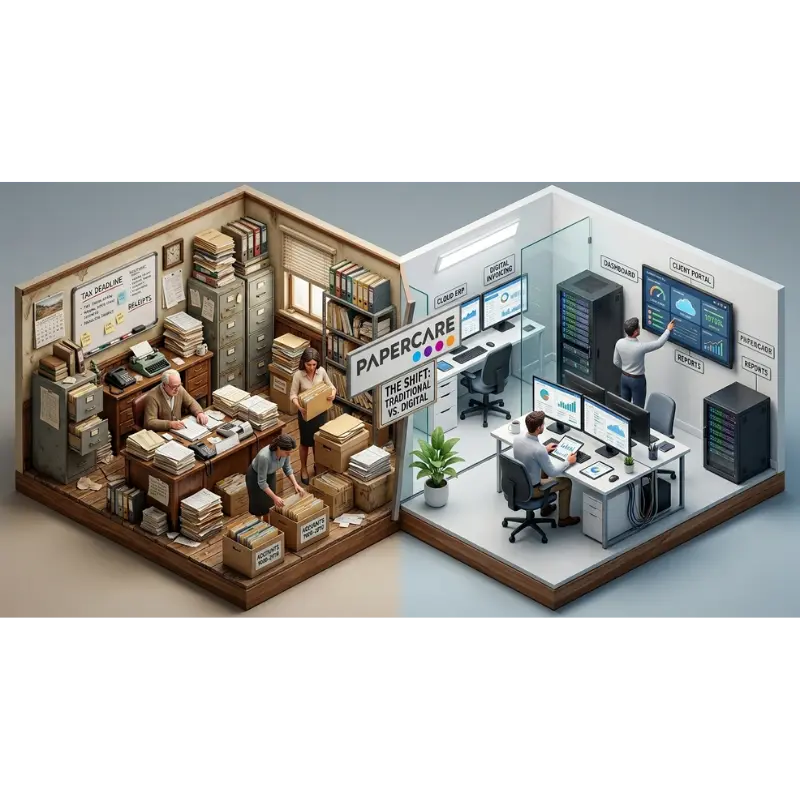

For decades, working papers have been at the centre of accounting workflows. They have supported compliance, documentation, and review processes across firms of all sizes. However, the way these working papers are created and managed has remained largely unchanged.

Many UK accounting firms still rely on spreadsheets, disconnected documents, and manual processes to manage their work. While this approach may have worked in the past, it is increasingly becoming a limitation in today’s environment.

As client expectations grow, deadlines tighten, and regulatory demands increase, traditional working papers are struggling to keep up. What was once a reliable system is now creating inefficiencies, reducing visibility, and limiting scalability.

Understanding why this shift is happening is critical for firms that want to remain competitive.

The Traditional Working Papers Approach

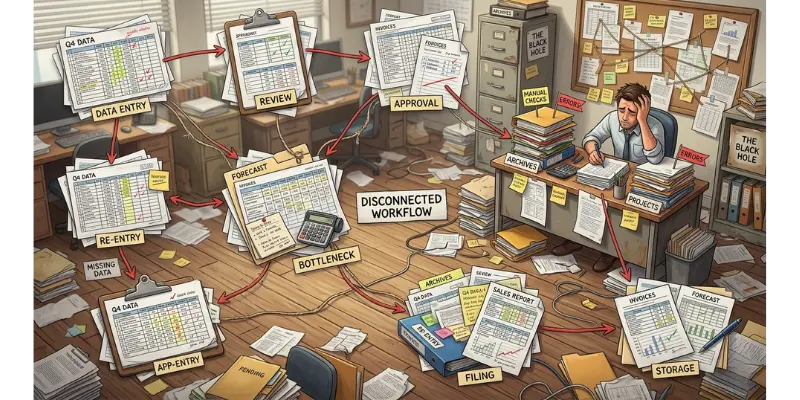

Traditional working papers are typically built around spreadsheets and manual documentation. Each engagement may involve multiple files, versions, and formats, often stored across different locations. This creates a fragmented workflow where:

- Data is duplicated

- Version control becomes difficult

- Collaboration is limited

- Errors are harder to detect

While experienced teams may learn to manage these challenges, the system itself remains inefficient. The issue is not with working papers as a concept, but with how they are implemented in traditional environments.

The Hidden Limitations of Traditional Systems

At first glance, traditional working papers may appear to function adequately. However, many of their limitations are not immediately visible. These include:

- Time lost in manual data handling

- Lack of real-time visibility

- Inconsistent processes across engagements

- Difficulty scaling operations

Over time, these inefficiencies compound. What starts as small delays or minor inconsistencies can grow into significant operational challenges. For firms handling increasing workloads, these limitations become more pronounced.

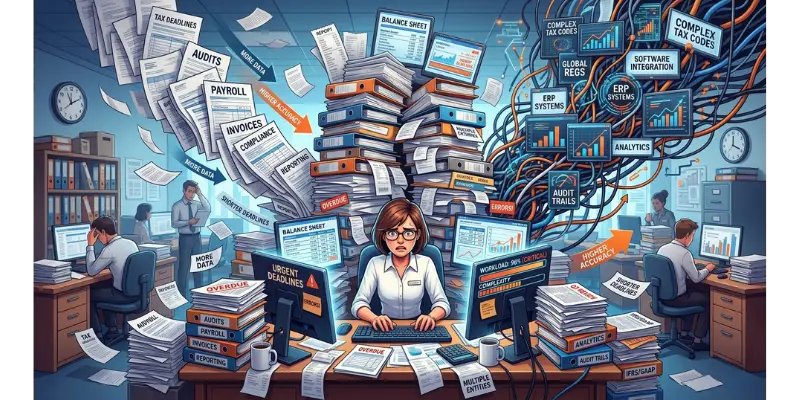

Why Modern Accounting Demands More

The accounting environment has changed significantly in recent years. Firms are now dealing with:

- Higher volumes of data

- More complex regulations

- Faster turnaround expectations

- Increased competition

In this context, workflows need to be:

- Faster

- More accurate

- More scalable

- More transparent

Traditional working papers struggle to meet these requirements because they were not designed for this level of complexity.

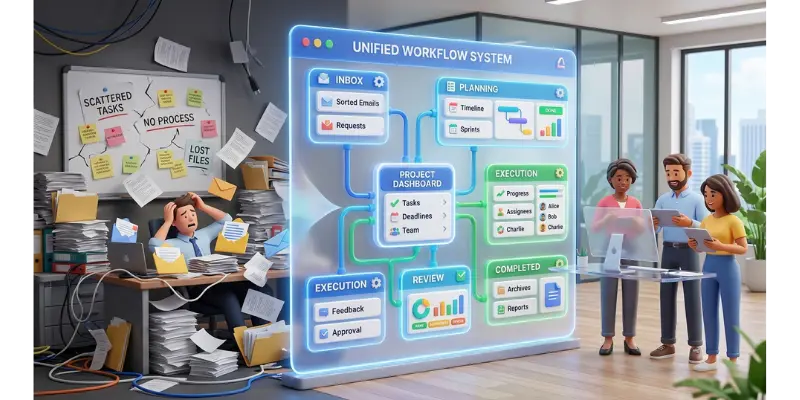

The Need for Structured Workflows

Modern accounting firms are moving towards structured workflows. This involves:

- Standardising processes

- Centralising data

- Creating consistent frameworks

Structured workflows reduce variability and make it easier to manage work at scale. They also create the foundation needed for automation and AI, which rely on consistency and clarity to function effectively.

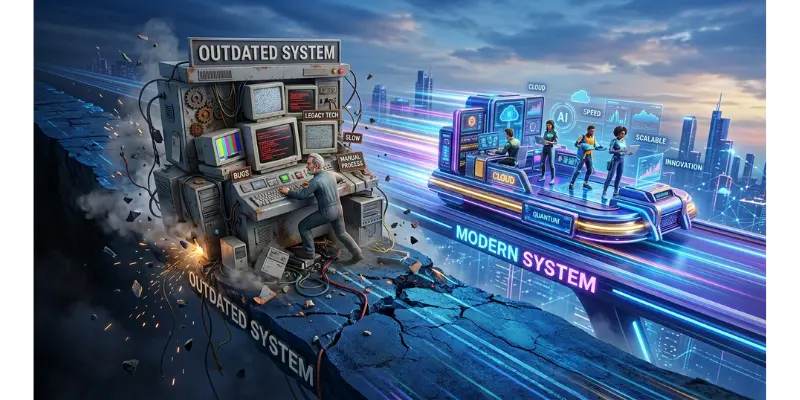

The Role of Technology in Transforming Working Papers

Technology is playing a key role in reshaping how working papers are managed. Modern systems bring together documentation, data, workflow tracking and collaboration tools into a single environment.

This eliminates many of the inefficiencies associated with traditional approaches and creates a more cohesive workflow. The focus is no longer on managing individual files, but on managing the entire process.

From Static Documents to Dynamic Systems

Traditional working papers are static. Once created, they do not adapt or provide additional insights. Modern systems, on the other hand, are dynamic. They allow:

- Real-time updates

- Integrated data flows

- Automated checks

- Continuous visibility

This shift changes how accountants interact with their work. Instead of managing documents, they manage systems.

How This Impacts Efficiency and Accuracy

Efficiency and accuracy are two of the most important outcomes of modern workflows. By reducing manual processes and introducing structured systems, firms can:

- Complete work faster

- Reduce errors

- Improve consistency

This not only benefits internal operations but also enhances client service. Firms can deliver work more reliably and with greater confidence.

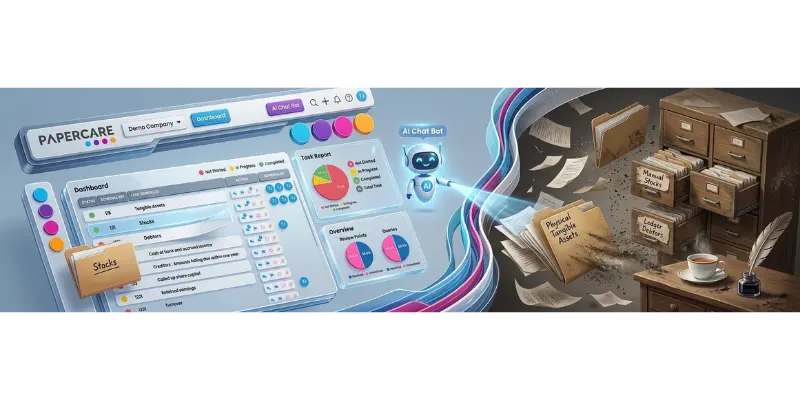

Where Papercare Fits Into This Transition

Platforms like Papercare are designed to address the limitations of traditional working papers.

By providing a structured, centralised environment, Papercare enables firms to:

- Standardise workflows

- Improve collaboration

- Integrate AI capabilities

- Gain real-time visibility

Rather than replacing working papers, it redefines how they are used. This allows firms to retain the benefits of working papers while eliminating the inefficiencies of traditional systems.

The Risk of Staying with Traditional Methods

Firms that continue to rely on traditional working papers face several risks. These include:

- Reduced efficiency

- Increased operational pressure

- Difficulty scaling

- Loss of competitive advantage

As the industry continues to evolve, these risks are likely to increase. Firms that do not adapt may find it harder to meet client expectations and maintain profitability.

The Future of Working Papers in Accounting

The future of working papers is not about eliminating them, but about evolving them.

Working papers will continue to play a central role in accounting workflows. However, they will be:

- More structured

- More integrated

- More intelligent

Technology will enable firms to move beyond manual processes and create systems that support efficiency and growth.

Conclusion

Traditional working papers have served the accounting profession well, but they are no longer sufficient for the demands of modern firms.

The shift towards structured, technology-driven workflows is not just a trend, it is a necessity.

Firms that embrace this change will be better positioned to handle increasing complexity, improve efficiency, and deliver greater value to their clients. Those that do not risk falling behind in an increasingly competitive landscape.